The PRIME Philippines 2025 Media Briefing on the Mid-Year Philippine Real Estate Outlook entitled “Turning the Tide: The Business Edge in Evolving Times,” was held on August 7, 2025 at 2:00 PM, at GreatWork, 32nd Floor, Mega Tower, Ortigas Center, Mandaluyong City.

In this in-person session, PRIME presented the following topics:

2025 Mid-Year Real Estate Market Performance

Property Market Outlook for the remainder of 2025 and beyond

This event is exclusively organized for their valued media partners, as they shared timely and relevant market perspectives with the press community.

PRIME Philippines has organized and hosted the event for their valued media partners, as they shared where Philippine real estate finds strength in 2025. They shared the Industrial Market Update (Clustering-effect defines the industrial demand in 2025); Office Market Updated (Where the next office boom begins – beyond the orbit of Metro Manila);and Retail Market Update (Reshaping Retial: Evolving Formats, New Occupiers, and Regional Growth);

PRIME Philippines recently organized and hosted the 2025 Media Briefing on the Mid-Year Philippine Real Estate Outlook entitled “Turning the Tide: The Business Edge in Evolving Times,” held on August 7, 2025 at 2:00 PM, at GreatWork, 32nd Floor, Mega Tower, Ortigas Center, Mandaluyong City.

The first half of 2025 tested the adaptability of the Philippine real estate market and the broader economy. While global headwind, including volatile U.S. trade policies, ongoing geopolitical conflicts, and tighter migration channels, tempered investor sentiment, the domestic market demonstrated measured resilience and pockets of growth.

Economic growth slows, but inflation relief and growing consumer expenditure give markets breathing room

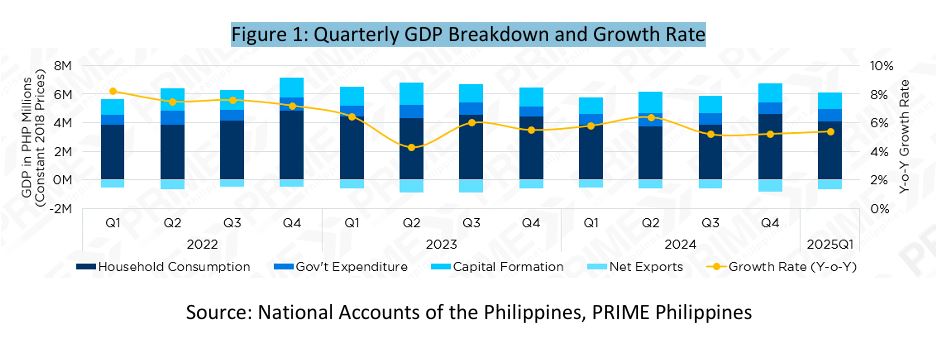

The macroeconomic path remained meandering but manageable. GDP growth slowed to 5.4 percent in the first quarter, weighed down by a 19.9 percent contraction in net exports, moderated private construction activity, and high base effects. Furthermore, growth forecasts from the Department of Budget and Management (DBM), International Monetary Fund (IMF), and Asian Development Bank (ADB) were trimmed considering persistent global uncertainty.

Even with this slowdown, the Philippines ranked second among ASEAN economies, tied with China, behind Vietnam’s 6.9 percent expansion. Despite global uncertainty, growth was sustained by domestic drivers. Household consumption rose 5.3 percent, supported by higher employment, easing inflation, and wage gains. The services sector, which accounts for over 60 percent of GDP, also expanded by 6.3 percent.

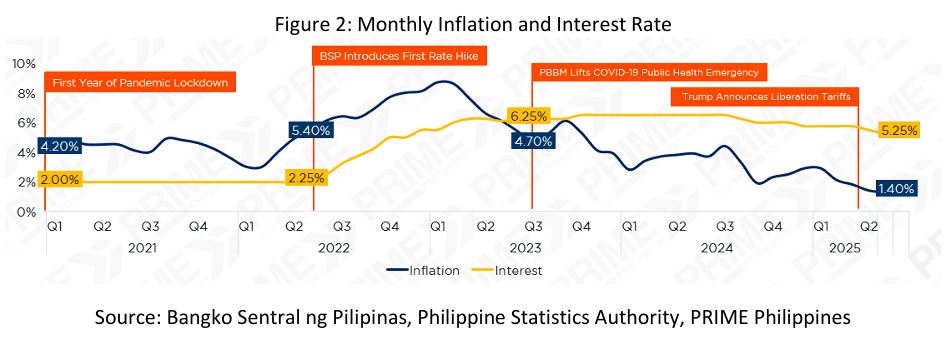

Beyond sustaining growth, the Philippines recorded an average inflation rate of just 1.8 percent in the first half, positively well below the BSP’s 2-4 percent target, driven by lower food and transport costs, rice tariff cuts, and favorable base effects. This gave the Bangko Sentral ng Pilipinas (BSP) room to reduce its policy rate twice this year to 5.25 percent, with further cuts in the pipeline if inflation stays low.

Overall, the combination of easing price pressures and rising domestic consumption hedges well against geopolitical uncertainty for the second half of the year, creating a supportive backdrop for real estate activity.

Metro Manila sees uneven office occupancy shifts across different business districts

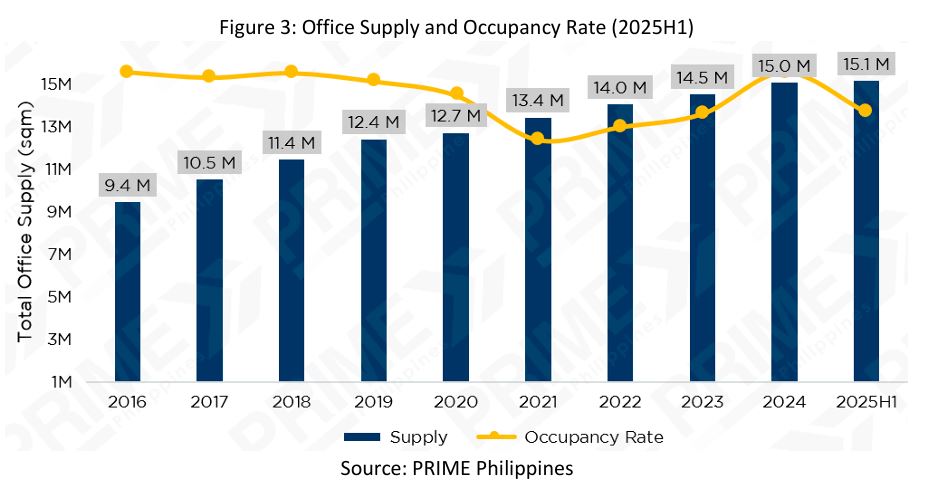

Metro Manila’s office market posted a mixed performance in the first half of 2025. While the National Capital Region (NCR) remains firmly in a tenant-driven market, Bonifacio Global City (BGC), Makati, and Ortigas registered year-on-year occupancy gains of zero to three percent, driven by expansions from Business Process Outsourcing (BPO) firms, professional services companies, and government relocations. By contrast, the Bay Area and Alabang recorded slight drops of 3.2 percent and 3.7 percent, respectively, as vacancies from the left overs of the Philippine Offshore Gaming Operations (POGO) and right-sizing of BPO and IT companies persisted. The lingering oversupply in these areas extends the time of the landlords to backfill the vacated spaces. With no new office stock in the NCR during the first half, and only 3% growth is expected for the remainder of the year, office landlords in Metro Manila can breathe a sigh of relief.

Rental performance reflected these trends. Metro Manila’s average lease rate fell six percent year-on year, with Pasay posting the steepest drop at 10.6 percent. Outside NCR, however, Davao’s rates rose 12.7 percent due to a shortage of Grade A PEZA-accredited spaces, while Metro Cebu saw a more modest 3.9 percent increase, in line with its recovery trajectory.

Government relocations and expansions signal latent office market support

Quezon City, on the other hand, presents an interesting case: despite strong interest from government agencies and professional service firms, its occupancy declined by 3.5 percent, as much of the government’s requirements remain in the procurement stage and have yet to convert into actual take up. Nonetheless, government agencies accounted for the majority or 18.5 percent of national office requirements in the first half, with interest concentrated in Quezon City, Pasay, and Pasig.

Many of these agencies, headquartered in the Manila and Quezon City, are seeking to relocate due to aging facilities or are expanding their footprints. This institutional demand provides a critical buffer, helping to hedge against potential contractions in expansions from the private sector and supporting the city’s resilience in the evolving office landscape.

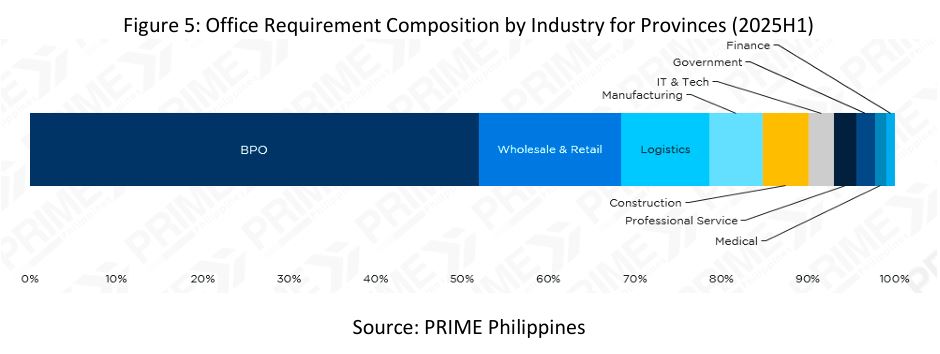

BPO expansions reinforce demand in CBDs and extend growth to provincial hubs

Following government interest, the BPO sector remained a key driver of office demand, accounting for 13.3 percent of the national total in the first half of 2025. In Metro Manila, most activity came from the expansion of existing operations in Central Business Districts (CBDs) such as BGC, Makati, and Ortigas, reflecting sustained demand from outsourcing firms serving global markets—particularly in finance, IT, and healthcare-related services.

Provincial hubs post strong gains on back of BPO interest and diversified demand

Beyond the capital, several regional hubs including Clark, Iloilo, Bacolod, and Davao registered notable growth, with much of the momentum coming from the continued expansion of BPO companies seeking lower-cost talent pools and reliable continuity sites. Metro Clark’s occupancy climbed 4.8 percent, supported by robust infrastructure, reliable connectivity, and generous fiscal incentives from investment promotion agencies such as the Clark Development Corporation (CDC), Philippine Economic Zone Authority (PEZA), and the Board of Investments (BOI).

Metro Cebu’s occupancy rose 8.1 percent, driven by flexible workspace demand and a resilient BPO base, complemented by growing interest from e-commerce, logistics, and shared services firms. The city’s steady growth is reinforced by ongoing Grade A office developments, strong infrastructure, and the expansion of both established and new entrants.

Outside these hubs, Iloilo is gaining traction through modern township developments and a growing talent pool, while Bacolod continues to attract BPO and healthcare firms, supported by its English-speaking workforce, lower operating costs, and competitively priced, repurposed office spaces offered by local developers.

Among the country’s major office hubs, Davao recorded the highest occupancy at 90 percent, with major BPO expansions offsetting the impact of minor dips from lease expirations and tenant exits linked to cost constraints, downsizing, or shifts to remote work. Its tenant mix also continues to diversify, with healthcare support, professional services, finance, education, and government offices expanding their presence.

Furthermore, shifts in tenant behavior continue to shape leasing patterns. In Davao, companies are increasingly seeking 150-700 square meter spaces to accommodate phased expansions or hybrid work setups. Flexible arrangements such as shorter leases, break clauses, and plug-and-play offices are becoming standard for new or scaling teams. Grade A buildings with PEZA accreditation, strong IT infrastructure, backup power, and good transport links remain preferred, although cost-conscious tenants are open to well-located Grade B options with efficient layouts.

Nationwide warehouse requirements surged 80%, with Bulacan at the forefront

Beyond offices, the industrial sector is charting its own growth trajectory, led by record warehouse demand. The industrial sector recorded one of its strongest half-year performances to date. Nationwide warehouse demand surged 80 percent to 691,900 square meters in the first half of 2025 compared to the second half of 2024, powered by wholesale and retail, logistics, and manufacturing activity.

Bulacan emerged as a standout, with the retail sector accounting for almost 83 percent of local requirements, equivalent to 13 percent of total national demand, reflecting its long-standing position as a preferred location for Metro Manila–based retailers seeking to strengthen their supply chains. Its strategic connectivity to the capital continues to make it highly attractive for distribution-focused tenants.

Cavite, meanwhile, has seen a notable shift in demand patterns. Manufacturing-related interest, which began tapering off in late 2024, has continued to soften as tenants favor Batangas for its larger land supply, lower costs, and proximity to major ports. In contrast, logistics demand in Cavite has remained stable, reinforcing its role as a last‑mile delivery hub and signaling its evolution from a balanced manufacturing–logistics base into a logistics‑anchored submarket.

On the other hand, Laguna has experienced a slowdown in new demand due to historically low vacancy rates, averaging below four percent, which have pushed some prospective tenants toward neighboring corridors such as Cavite and Batangas. Even so, its 97.77 percent occupancy rate, sustained by long‑term tenants with high renewal rates, underscores its enduring relevance as a manufacturing and logistics hub.

Seasonal demand patterns mirror strategic planning and operational cycles

This surge in demand is reinforced by distinct seasonal patterns, with both wholesale and retail, and logistics requirements typically peaking in the first (Q1) and last (Q4) quarters of the year, albeit for different reasons. For wholesale and retail firms, these periods align with long-term network expansion and supply chain strategies, often tied to annual or biannual business planning cycles, resulting in research done early or late in the year. For third-party logistics (3PL) providers, the same quarters see heightened short-term leasing activity to manage inventory surges during major sales periods and holidays. At the same time, local tenant preferences are shifting toward consolidated, strategically located warehouses over dispersed networks, as companies work to streamline their supply chains and reduce transport inefficiencies.

These concurrent peaks create a cyclical rhythm in the warehousing market, leaving the second (Q2) and third (Q3) quarters relatively subdued. Across these cycles, demand remains anchored in three sectors: wholesale and retail, transportation and logistics, and manufacturing—fueled by e‑commerce growth, the expansion of 3PL networks, and steady requirements from export‑oriented electronics manufacturers.

Green tech surge and policy incentives position Philippines as emerging manufacturing hub

Manufacturing added further depth to demand in the first half, with 81,000 square meters of requirements from computer, electronics, and optical product makers, particularly in green technology such as solar components, EV batteries, and energy systems. A sharp rise in green tech production in 2025 may signal the early stages of a broader tech manufacturing expansion, positioning the Philippines as an emerging hub for clean, export-oriented industrial activity in Southeast Asia. Heightened US-China trade tensions, especially tariffs on Chinese-made microchips and semiconductors, have accelerated supply chain diversification, prompting global manufacturers to consider the Philippines under the China+1+1 strategy.

The country’s competitiveness in attracting high-value manufacturing is being strengthened by the CREATE Law, Green Lane Services, and PEZA’s proactive facilitation of ecozone registrations. Strategic locations such as Clark, Subic, and Batangas, with their logistical connectivity, utilities readiness, and skilled labor pools, are expected to see heightened interest for build-to-suit manufacturing facilities and specialized warehouse clusters.

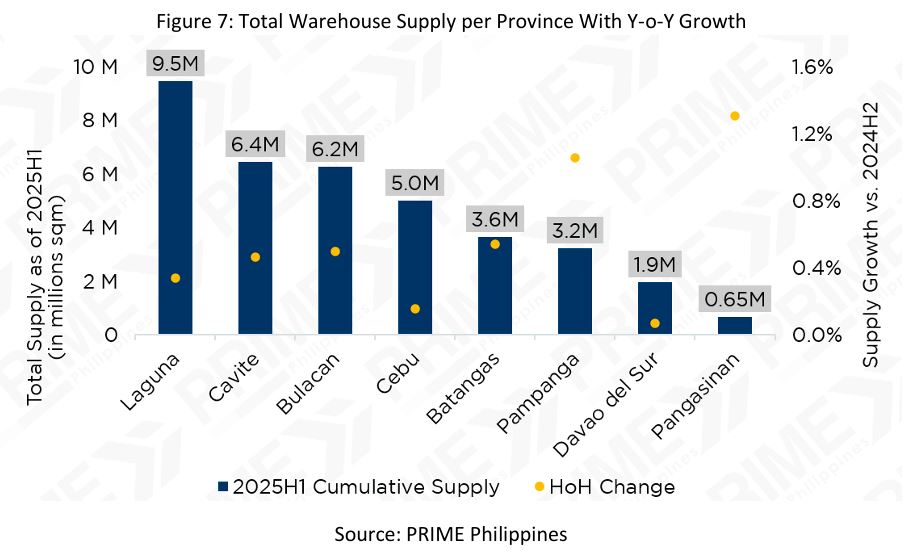

Fortunately, the growth of warehouse supply has responded swiftly to burgeoning demand. From the second half of 2024, warehousing stock nationwide expanded by approximately 1.5 million square meters, and the momentum shows no signs of slowing. As of the first half of 2025, 3.98 million square meters of land for upcoming warehouse construction has been recorded, with a substantial share concentrated in Tarlac through projects such as Tari Estates and New Clark Estates.

Towards the north, Pampanga also remains a key focus for developers, particularly in Mabalacat, Angeles, Porac, and San Fernando, owing to its established industrial parks and excellent connectivity via NLEX and MacArthur Highway. Pangasinan, while still without a notable pipeline beyond a few major projects, is increasingly viewed as the next northern industrial province after Pampanga and Bulacan. In Bulacan, the pipeline is concentrated in Bocaue and Sta. Maria, locations that take advantage of proximity to Metro Manila while mitigating flooding risks present in other parts of the province.

In the south, Cavite’s development hotspots continue to be General Trias, Carmona, and Silang, where connectivity to SLEX, CAVITEX, and CALAX sustains their industrial appeal despite congestion challenges. Cebu is also contributing to the supply base, with developments such as DoubleDragon’s Centralhub adding to the country’s growing network of strategically located warehouses.

Elevated occupancies persist as warehouse demand and expansion stay in balance

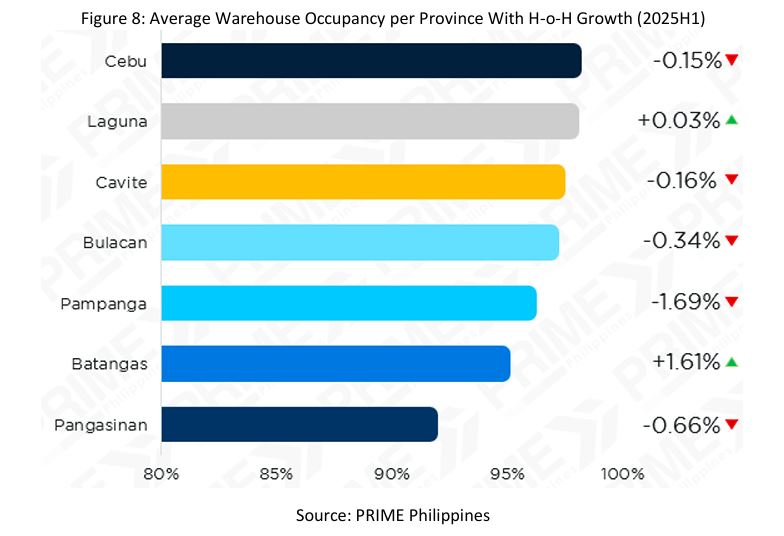

Given the equilibrium of blossoming demand and aggressive expansion for warehousing, occupancies are expected to continue prospering. Cebu led the country with an industrial occupancy rate of approximately 98 percent in the first half of

This performance is expected to continue, supported by the upcoming delivery of 50,000 square meters of warehouse stock by end‑2025, which should help absorb pent‑up demand driven by resilient logistics and e‑commerce activity. Moving forward, a growing number of tenants and developers have been relocating or expanding toward Liloan and Consolacion, creating a new industrial hotspot to bypass congestion and warehouse saturation in central nodes like Mandaue.

In Luzon, Laguna maintained a solid 97.77 percent occupancy despite a recent dip in new leasing inquiries and developer interest, with stability underpinned by a base of long‑term tenants, high renewal activity, and swift re‑absorption of vacated spaces, often within weeks.

Pangasinan is another very promising province. With a 91.6 percent occupancy, it primarily benefits from its proximity to the Tarlac‑Pangasinan‑La Union Expressway (TPLEX) and Central Luzon Link.

Expressway (CLEX). While internal demand remains limited, interest from Fast Moving Consumer Goods (FMCG) companies has increased as they seek to extend their reach into northern provinces.

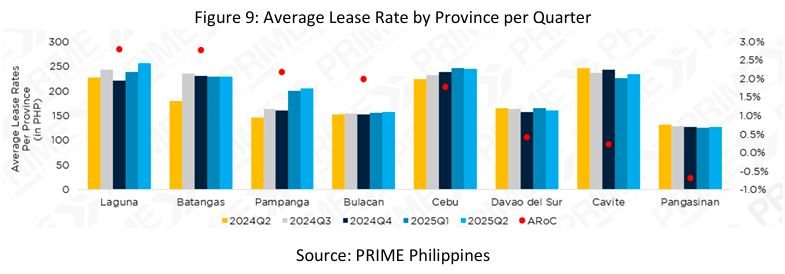

Despite these developments, warehouse lease rates have remained broadly stable, with most provinces posting an average rate of change of zero to two percent in recent quarters. The main exceptions were Pampanga, where rates climbed 25 percent in the first quarter following the introduction of premium warehouses in San Fernando and Mexico, and Laguna, where select high‑spec facilities drove a 7.6 percent increase in the second quarter. Aside from the two, this modest pace of growth reflects the prevalence of long‑term lease structures and the natural lag between price adjustments and the pass‑through of inflationary costs.

Retail demand strengthens with diverse formats and wider geographic reach

In step with the industrial market’s stability, retail demand continues to build, with food and beverage operators leading expansion.

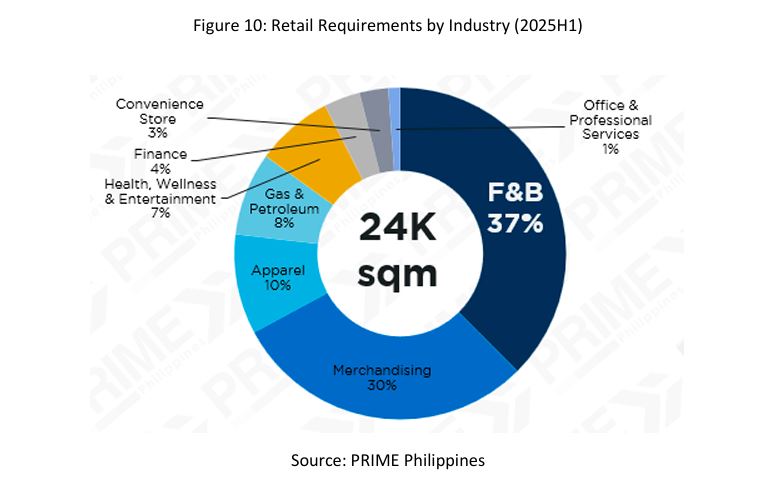

Retail demand in the first half of 2025 remained anchored by robust food and beverage (F&B) activity, which accounted for 37 percent of total requirements, with 51 percent of this demand coming from outside Metro Manila. While mall formats remain a mainstay, many major chains continue to seek standalone lots, valuing the flexibility they offer in brand identity, space optimization, and customer experience. The ability to integrate drive‑thru facilities is a particularly sought‑after feature, enabling operators to capture both foot and vehicular traffic. However, a more careful and strategic approach to F&B expansion has emerged, with operators placing greater emphasis on the strategic value and suitability of a location rather than simply increasing outlet numbers.

Beyond the established brands, smaller players and start‑ups are carving out a niche by turning restaurants into destinations in themselves, most notably through “Instagrammable” cafés that blend dining with experiential design. Convenience stores and many F&B brands are also adopting an alternative positioning strategy by locating near residential communities, tapping into built‑in foot traffic and repeat customers.

Rising middle class drives lifestyle retail and omnichannel growth

Beyond F&B and neighborhood‑oriented concepts, the retail upswing is being reinforced by rising consumption for non-essential goods. General merchandising accounted for 30 percent of retail demand, underpinned by a growing middle class and stronger household spending. Rising incomes and improved purchasing power are driving demand not only for essentials, but also for lifestyle products in fashion, beauty, and technology.

E‑commerce platforms such as Shopee, Lazada, TikTok Shop, and Instagram have also conditioned consumers to value visual presentation, product curation, and trend‑driven merchandising. This digital exposure is influencing offline retail, pushing physical stores to match the curated, urgency‑driven feel of online shopping. Retailers are responding through merchandising strategies that enhance brand storytelling, create scarcity cues, and encourage impulse purchases.

This growing interplay between online and offline channels is blurring the boundaries of retail, with physical stores increasingly designed to complement digital touchpoints. As a result, hybrid models such as buy‑online‑pick‑up‑in‑store (BOPIS) and research‑online‑purchase‑offline (ROPO) have moved from optional conveniences to standard practice.

Online native brands are also expanding into brick-and-mortar locations to strengthen brand legitimacy and provide immersive product experiences. Beauty and lifestyle labels such as Sunnies Face and BLK Cosmetics have transitioned from digital first platforms to mall-based boutiques, echoing global trends seen in brands like Glossier and Warby Parker. Philippine mall developers are also adapting to this by curating zones for these direct-to-consumer popups, integrating them into the country’s enduring mall culture.

Rising EV adoption opens new frontiers for supporting retail infrastructure

Alongside the rise of e‑commerce, another major shift is reshaping the retail landscape. The growth of electric vehicles is creating new spatial requirements for retail, both as a service offering and as a traffic driver. EV sales in the Philippines grew from under 2 percent of total vehicle sales in 2023 to nearly 4 percent in 2024, with CAMPI projecting a rise to 4-5 percent in 2025. This momentum is supported by national policy, particularly Executive Order No. 12, which removes tariffs on battery electric vehicles and key components for five years, and by the Public Utility Vehicle Modernization Program’s push for fleet electrification.

Infrastructure growth has been rapid: as of March 2025, the DOE reported 912 public charging stations nationwide, up from fewer than 300 in 2023, with a target of 7,300 by 2028. Malls have been central to this rollout. SM Supermalls has deployed chargers in 69 malls, Ayala Malls in 31 locations, Robinsons Malls in four flagship properties, and Megaworld Lifestyle Malls in key urban centers. These installations are being positioned not only as sustainability features but also as amenities that enhance tenant attraction and customer dwell time.

Private operators are also scaling up. VinFast is launching over 100 EV service centers nationwide with JIGA Philippines, while logistics firm Mober opened the country’s largest commercial EV charging hub in Pasay in March 2025, with plans for two more mega‑hubs in Bulacan and Laguna.

Regional markets are joining the network, according to the Department of Energy (DOE), Cebu now hosts 14 charging points, Davao has at least seven, and the Bicol Region has installations in Legazpi, Naga, and Sorsogon, reflecting the broadening reach of EV infrastructure beyond Metro Manila.

Strong fundamentals signal Davao’s rise as a key retail destination

Beyond sector wide shifts, retail growth is also shaped by location specific dynamics, with some markets benefiting from distinct economic and demographic strengths. Davao is one such market, showing steady activity supported by strong fundamentals.

Davao’s strong macro and demographic profile continues to underpin its position as one of the most promising retail markets in the country. In the first half of 2025, it accounted for 47 percent of all provincial retail requirements, supported by its status as Mindanao’s largest economy and by having the highest GDP per capita in the island group. Its 1.85 million residents make it the most populous city outside Metro Manila, with a demographic skewed toward a large working population and a growing base of young dependents, both of which support long‑term consumption growth.

These fundamentals translate into diverse retail opportunities. Culturally, Davao consumers balance practicality with openness to innovation, creating demand for offerings that enhance convenience, wellness, and family life. This has fueled interest in food parks, wellness centers, and lifestyle‑oriented retail spaces. In fact, health and wellness tenants alone accounted for 40 percent of retail inquiries in H1 2025.

While prime malls such as SM Lanang and Abreeza remain strong anchors for new entrants, secondary districts have experienced slower lease‑up, giving tenants greater negotiating leverage. Co‑location strategies remain important, with brands often launching alongside established anchors like Mercury Drug, Jollibee, and Uniqlo to capture spillover traffic. Looking ahead, growth corridors such as Toril, Mintal, and Buhangin are gaining traction, supported by infrastructure upgrades and expanding residential communities.

Market outlook: Emerging demand corridors point to targeted growth opportunities

Across all sectors, emerging demand corridors are shaping the next wave of opportunities. For the office sector, the conversion of pending public sector relocations in NCR could lift occupancy, while provincial BPO growth is set to continue in Clark, Cebu, Davao, Iloilo, and Bacolod. In the industrial market, Tarlac, Pangasinan, and Pampanga are poised to lead warehousing supply growth, with high-value manufacturing benefitting from global trade realignment and lease rates expected to post modest gains. In retail, expansion will follow suburban and mixed-use developments, with health and wellness and food and beverage remaining key demand anchors, and EV infrastructure integration emerging as a competitive differentiator for malls and as a boon for land lessors.

Real estate performance in the first half of 2025 suggests a market not merely weathering global turbulence but actively repositioning to align with structural and geographic shifts in demand. While macro conditions remain fluid, the direction of change is clear decentralization, flexible formats, and responsiveness to innovation will define the most competitive opportunities in the months ahead.

About PRIME Philippines

PRIME Philippines is the country’s fastest-growing and most disruptive commercial real estate advisory firm. Established in 2013, PRIME has redefined the brokerage industry by replacing outdated practices with innovation, data intelligence, and relentless execution. With full-service offices in Manila, Cebu, and Davao, PRIME has completed over 300 high-impact projects nationwide. Backed by a team of over 100 professionals, PRIME is multi-awarded and trusted by the country’s top developers, investors, and occupiers. It is involved in big ticket office transactions and holds the No. 1 position in industrial leasing nationwide.